How Much Can You Save by Bundling Home and Auto Insurance?

In Washington, this is more common than in most states. Unbundling can outperform any bundle here — particularly because of the strength of regional carriers like PEMCO.If you own both a home and a vehicle, you’ve likely heard that bundling your insurance policies can save money.

But how much can you actually save?

Is it $50 a year? $500? Or is the discount mostly marketing language?

The real answer depends on your profile. But in many cases, homeowners save between 10% and 25% when bundling home and auto insurance.

Let’s break down what that really means in dollar terms.

What Is a Home and Auto Insurance Bundle?

Bundling means purchasing both your homeowners insurance and auto insurance from the same company.

In return, insurers apply a multi-policy discount to one or both policies.

If you’re unfamiliar with how bundling works, you can read our full breakdown here: Home and Auto Insurance Bundle: Is It Actually Cheaper in Washington? and Pros and Cons of Bundling Home and Auto Insurance.

Now let’s talk numbers.

Average Savings From Bundling Insurance

Most major insurers advertise bundle discounts between:

10% and 25%

But the percentage alone doesn’t tell you much.

What matters is:

Your current premiums

The insurer’s base rates

Your location

Your claims and driving history

Let’s look at realistic examples.

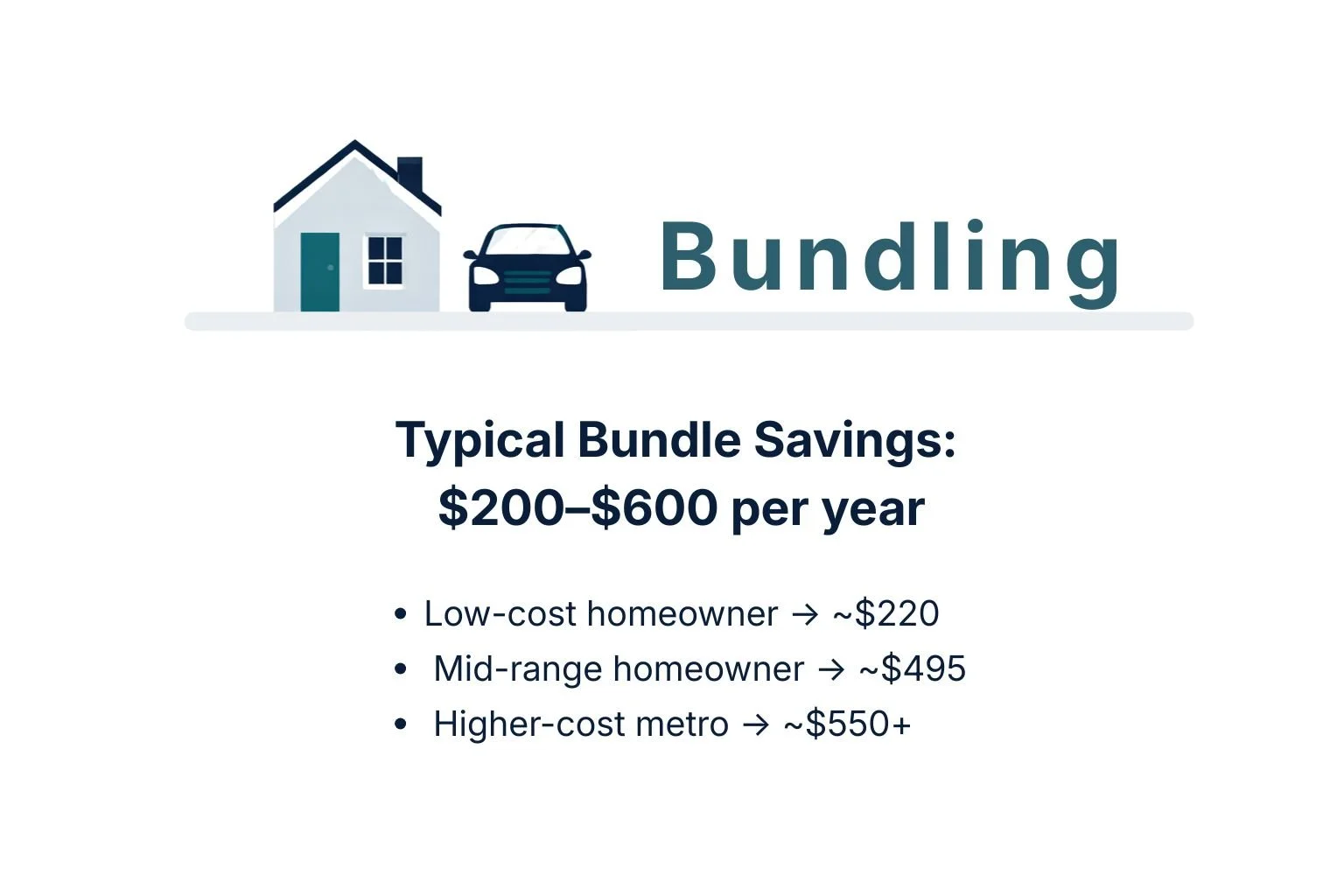

Example 1: Moderate-Priced Homeowner

Home Insurance: $1,500/year

Auto Insurance: $1,800/year

Total Separate Premium: $3,300/year

With a 15% bundle discount applied across policies:

Estimated Savings: ~$495/year

New Total: ~$2,805/year

That’s meaningful savings.

Example 2: Higher-Cost Metro Area

Home Insurance: $2,200/year

Auto Insurance: $2,400/year

Total Separate Premium: $4,600/year

With a 12% effective discount:

Estimated Savings: ~$552/year

New Total: ~$4,048/year

Even smaller percentages can produce larger dollar savings when premiums are higher.

Example 3: Low-Risk, Low-Cost Scenario

Home Insurance: $1,000/year

Auto Insurance: $1,200/year

Total Separate Premium: $2,200/year

With a 10% discount:

Estimated Savings: ~$220/year

New Total: ~$1,980/year

Still valuable, but a smaller savings.

Why Savings Vary So Much

Insurance pricing is dynamic and state-specific.

Savings depend on:

ZIP code risk modeling

Replacement cost of your home

Driving record

Credit-based insurance scoring (where allowed)

Claims history

Coverage limits and deductibles

In some states, bundling discounts are more aggressive because insurers compete heavily for multi-policy customers.

In others, base rates may already be low, reducing discount impact.

The Hidden Factor: Base Rate Competitiveness

Here’s something most comparison sites won’t emphasize:

The discount percentage is not what determines savings.

Base rates do.

If one insurer offers:

Higher base premiums

Larger discount

It may still be more expensive than:

Lower base premiums

Smaller discount

The only way to know is to compare total annual cost.

Not just advertised savings.

Is Bundling Always the Cheapest Option?

No.

Sometimes you can save more by:

Placing home insurance with Carrier A

Placing auto insurance with Carrier B

Especially if one company specializes in one line of coverage.

That’s why the smartest move isn’t automatically bundling.

It’s comparing.

In Washington, this is more common than in most states. Unbundling can outperform any bundle here, particularly because of the strength of regional carriers like PEMCO.

How Often Should You Re-Compare Bundled Insurance?

Even if you’re already bundled:

Re-shop every 1–2 years.

Why?

Risk models change

Carriers adjust pricing

New competitors enter markets

Loyalty pricing can increase over time

Many homeowners overpay simply because they haven’t compared recently. See how the top bundle carriers compare in Washington.

When Bundling Typically Saves the Most

Bundling often produces stronger savings if:

You have a clean driving record

You haven’t filed recent home claims

You own a mid-to-high value home

You live in a competitive insurance market. Washington is one of those markets. PEMCO's pricing structure makes it worth getting a regional quote before assuming a national carrier's bundle is your best option.

You’re not currently shopping aggressively

For stable homeowners with both policies, bundling is frequently a strong starting point.

How to Compare Bundle Savings the Right Way

If you’re evaluating your options, follow this process:

Get bundled quotes from multiple insurers.

Get separate quotes for home and auto.

Match coverage limits exactly.

Compare total annual premium.

Review deductibles and exclusions.

If you decide to switch after comparing, here's how to do it without creating a coverage gap.

The goal isn’t the biggest percentage discount.

The goal is the lowest total cost for the right coverage.

Before comparing rates, it's worth knowing whether your current coverage is actually doing its job.

Take the free coverage checkup → 2 minutes. No personal info required.

Final Answer: How Much Can You Save by Bundling Insurance?

Most homeowners save somewhere between $200 and $600 per year.

But your exact savings depend on:

Your home’s value

Your driving record

Your state

Your insurer

Bundling is often worth comparing, especially if you haven’t reviewed your rates in the past couple of years.

Insurance pricing changes regularly. Comparison shopping brings clarity.

Frequently Asked Questions (FAQs)

-

Most savings fall between 10% and 25%, which often translates to $200–$600 annually depending on premium size.

-

No. Sometimes separate policies from different insurers produce lower total premiums.

-

Bundling doesn’t automatically change coverage, but policy limits and deductibles should always be reviewed when comparing options.